Issuer Login

Manage your cap table, view shareholder reports, shareholder meeting voting, transactions, update information securely.

Shareholder Login

View your stock holdings, employee plan and options, transactions, and update contact information securely

Vote Proxy

View shareholder meeting materials and vote your shares securely.

Learn More

Learn more about our cap table management and transfer agent services.

IPO Transactions

Financing/IPO Transactions – February 2024

Financing/IPO Transactions – January 2024

Financing/IPO Transactions – December 2023

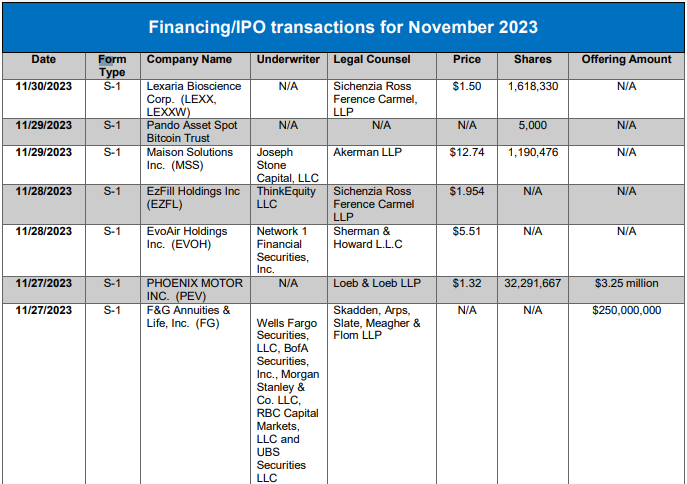

Financing/IPO Transactions – November 2023

Financing/IPO Transactions – October 2023

Media

Popular Top 10

Categories